|

| Russ Roberts |

Russ is a very good interviewer, and the EconTalk series quite interesting.

|

| Russ Roberts |

the employees of a hotel who earn pretty much the same wage ... will be forced to have an expensive family plan... the ObamaCare mandate amounts to about a $10,000 burden on these businesses and by extension their employees.This leads to a novel (to me) economic effect.

As businesses discover that almost everyone who earns less than the average wage gets a better deal ...in the exchange or from Medicaid, and that most people who earn more than the average wage get a better deal if insurance is provided at work, trends already evident will accelerate. Higher-income workers will tend to congregate in firms that provide insurance. Lower-income workers will tend to work for firms that don't. But efficient production requires that firm size and composition be determined by economic factors, not health-insurance subsidies.And John is prescient on just why exchange policies seem to be pretty awful:

Under ObamaCare, insurers are required to charge the same premium to everyone, regardless of health status, and they are required to accept anyone who applies. This means... they have strong incentives to attract the healthy (on whom they make a profit) and avoid the sick (on whom they incur losses).

The result has been a race to the bottom in access and quality of care. To keep premiums as low as possible, the insurers are offering very narrow networks, often leaving out the best doctors and the best hospitals.He has some nice alternatives, including

giving everyone the same universal tax credit for health insurance would be a good start. More easily accessible health savings accounts for people in high-deductible plans is another good idea.

Every provision in ObamaCare that encourages employers either not to hire people or to reduce their hours should go. Everything in the law that prevents employers from providing individually owned health insurance that travels from job to job should go. And everything that makes HealthCare.gov more complicated than eHealth (a 10-year-old private online exchange) should go.By contrast, I was interested that Emanuel, an architect of the law, was so weak in its defense.

Look at access to care. According to Gallup, the percentage of uninsured Americans declined from 18% in the middle of 2013 to 15.9% in the first quarter of 2014..Interesting that pro and con opeds start with essentially the same opening sentence! The glass is indeed 85% empty. Ezekiel passes on the canard that health insurance is "access to care."

Look at quality. In 2010, as part of the Affordable Care Act, the federal government launched the Partnership for Patients, a push to reduce infections and other preventable errors and injuries that occur in hospitals through financial incentives. The results have been dramatic. In three years, avoidable central line infections have dropped 41%. Ventilator-induced pneumonias have dropped 55%. Unnecessary, elective C-sections have dropped more than 50%. Hospitals are also getting better at preventing falls, which have declined more than 11%. Overall, the Partnership for Patients has prevented roughly 15,000 deaths, averted hundreds of thousands of injuries, and saved more than $4 billion.This was news to me. And astonishing. After all these years of complaining that doctors are too careful because of out-of-control liability, it took a Federal program to get doctors to wash their hands and prevent falls?

Step one would be to operate the exchanges like a cutting-edge e-commerce website, not a traditional government program. ...The challenge is more than getting the sites to work faster and more reliably. The challenge is to get them to run like Zappos or REI, with a relentless focus on improving the insurance offerings, attracting customers, and facilitating an easy, informative shopping experience.I just love this paragraph. It's written in a strange new voice that takes over policy discussions -- the regulatory passive. "to operate..getting the sites to work... to get them to run...." Just who is going to do all this toing? News flash: the ACA is a "government program," and it's run by Health and Human Services? When did government programs ever not operate like, well, government programs? When did any government program relentlessly "focus on improving the insurance offerings, attracting customers, and facilitating an easy, informative shopping experience." Try the Post Office some day. But no,

..there must be constant improvement. And it can probably occur only with a 21st-century, private-sector management structure—one that empowers a CEO, probably with health-insurance experience, and a team of tech-savvy management specialists, to run the entire operation.

Step two would be to change the way doctors and hospitals are paid as quickly and efficiently as possible. In order to control costs and improve quality, there needs to be a transformation in the way care is delivered. There needs to be continuous monitoring of patients in order to intervene early to prevent acute exacerbations of chronic illnesses. And when patients do get sick, there needs to be a greater focus on treating them outside of the hospital so the care they receive is safer, more efficient and lower-cost.

Now is not the time for autopilot. Lawmakers need to enhance the exchanges and more rapidly adopt alternatives to the fee-for-service payment system.This actually calls for legislative and regulatory changes no smaller than what Goodman calls for!

...all else being equal, monetary policy should be less accommodative--by which I mean that it should be willing to tolerate a larger forecast shortfall of the path of the unemployment rate from its full-employment level--when estimates of risk premiums in the bond market are abnormally low.This view has put Stein a bit in the camps of the hawks, meaning simply those who for one reason or another think the time to raise rates is sooner rather than later.

How, if at all, does monetary policy influence the evolution of the ratio? Without an answer to this question, it is hard to say how much one would want to alter the stance of policy when, say, the ratio is abnormally high relative to trend.He concludes that the Fed should watch risk premiums -- the expected excess return on long term treasuries and corporates -- and be ready to tighten if risk premiums seem too low. Essentially, the Fed should add a new term to the Taylor rule,

As an illustration, consider the period in the spring of 2013 when the 10-year Treasury yield was in the neighborhood of 1.60 percent and estimates of the term premium were around negative 80 basis points (3). Applied to this period, my approach would suggest a lesser willingness to use large-scale asset purchases to push yields down even further, as compared with a scenario in which term premiums were not so low.But measuring the term premium is tricky stuff. It's not just the spread between long bond and short bond yields. If long bonds are 1.60% and short bonds are 0%, it might just be that everyone expects interest rates to rise in the future, and expected returns are the same for holding any type of bond. The "risk premium" is how much of that spread exists over and above (or in this case, under and below) people's expectations of rising interest rates.

The 10-year nominal rate hit 1.63 percent on May 2, 2013. An estimate of the term premium based on the oft-cited methodology of Kim and Wright (2005) was negative 0.78 percent on this day.OK, how do Kim and Wright come to this conclusion? Basically, by running regressions. They (we) examine, in the past, what configuration of bond prices and other variables have been followed by interest rate rises ("expectations hypothesis"), and what configuration has been followed by good returns to bond investors ("risk premium")?

Of course, there are many caveats. Foremost among them is the fact that the ability of increases in the EBP ["excess bond premium"] to predict future economic activity may not reflect a causal link from the former to the latter. Perhaps there are economic slowdowns that are caused entirely by nonfinancial factors, and, when investors see one on the horizon, they get skittish, causing the EBP to rise. If so, it would be wrong to conclude that easy monetary policy--even if it does, in fact, cause lower risk premiums--has any causal effect on the probability of a future slowdown. So at this point, the evidence that I have reviewed can only be thought of as suggestive.

Making progress on these difficult issues of causality will likely require a clearer articulation of the underlying mechanism that leads to such pronounced asymmetries in the relationship between credit spreads and economic activity. If a causal link is, indeed, present, what is there about it that leads increases in spreads to have a much stronger effect on the economy than decreases? I suspect that the answer has to do with something that mimics the effect of leveraged losses to financial intermediaries--and the attendant effect on credit supply. For example, GZ document that their EBP measure is closely correlated with the credit default swap spreads of broker-dealer firms. The reason could be that losses on their inventories of risky bonds erode the capital positions of these firms, which might in turn compromise their ability to provide valuable intermediation services. Alternatively, a similar mechanism may play out with open-end bond funds, whereby losses cause large outflows of assets under management, again compromising the intermediation function and aggregate credit supply.So, if there is a correlation between the level of the short rate, the term premium and the risk premium, and a correlation between those and financial stability, it's not about fundamental business cycle risk, it's something about frictions in the intermediation system. We are awfully far from understanding that process, and especially understanding it well enough to manipulate it!

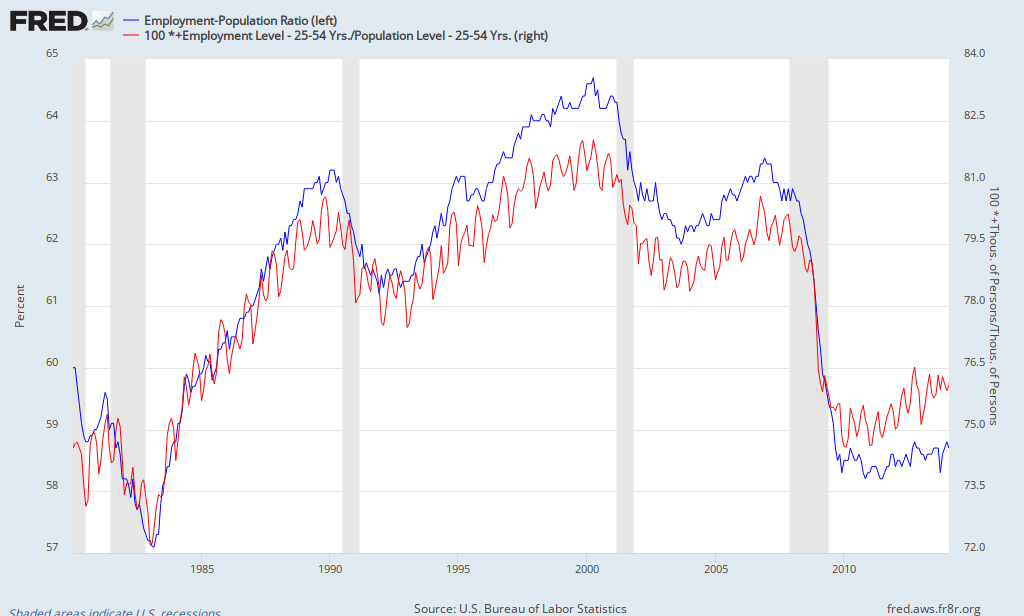

...let me emphasize the conjectural nature of these remarks. Even if this broad way of thinking about the problem turns out to be useful, there is a ways to go--in terms of modeling and calibration--before it can be used to make quantitative statements. Thus, at this early stage, I would not want to claim that one is likely to get policy prescriptions that differ significantly from those of our standard models. We will have to do the work and see what emerges.But understanding all this will take years. Do we really get to wait? Is Stein really making speeches to spur a decade long research agenda? Given the equally tenuous theorizing on the "dove" side about the relation between low interest rates and long-term unemployment or the employment-population ratio, should it wait? How should the Fed act with so much uncertainty about basic cause and effect? I'm glad I'm not on the hot seat.

...one of the central and most widely shared ideas in the academic finance literature is the importance of time variation in the risk premiums (or expected returns) on a wide range of assets. At the same time, canonical macro models in the New Keynesian genre of the sort that are often used to inform monetary policy tend to exhibit little or no meaningful risk premium variation. Even if most of the specifics of what I have had to say in this talk turn out to be off base, I have to believe that our macro models will ultimately be more useful as a guide to policy if they build on a more empirically realistic foundation with respect to the behavior of interest rates and credit spreads.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. ... asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments.

With the unemployment rate nearing 6-1/2 percent, the Committee has updated its forward guidance.In other words, the committee will do whatever it feels like doing, whenever it feels like doing it, based on whatever information it decides is relevant. The Committee updated its forward guidance by throwing it under a bus, or at least by clarifying that it is of the form "here is what we think now we will want to do in the future, but we can change our minds at any time."

Voting against the action was Narayana Kocherlakota, who supported the sixth paragraph, but believed the fifth paragraph weakens the credibility of the Committee's commitment to return inflation to the 2 percent target from below and fosters policy uncertainty that hinders economic activity.Narayana is always interesting. The fifth and sixth paragraphs are the ones I quoted above. Narayana wants more rules and commitments. But... from the dovish side! He's worried people don't know the Fed wants more inflation.

Fiscal policy is restraining economic growth,This must be a joke. Oh, no, I get it, the Fed has woken up to the growth-sapping effects of high marginal tax rates and a chaotic code. I wish.

|

| Source: Institutional Investor |

|

| Source: Journal of Political Economy |

|

| Source: Samuel Kapon and Joseph Tracy |

|

| Source: New York Times |

Much of the literature I have reviewed uses the same basic idea: Certain demographic groups have a certain propensity to participate in market work, and one of the main things we need to do as economists is project the number of people in each of these groups in order to determine a reasonable estimate of the expected (or “normal” or “trend”) labor force participation rate in the U.S. economy. Much of the literature concludes that demographics have contributed substantially to the observed decline in U.S. labor force participation since 2000.

Still, the literature as a whole is a bit hollow. Simply saying that people in certain demographic groups tend to make the participation decision one way or another does not do enough to analyze the incentives of household labor supply decisions. The more we know about the details of the household labor supply choices, including choices to participate in market work, the better we can predict the impact of policy on labor force participation. Furthermore, we would like these decisions to be part of the macroeconomic model, as Erceg and Levin suggest.Here Jim speculates about the recent, and very worthwhile literature on "household production" that models the decision to work or not. He does not speculate on how much those decisions are distorted by policy. 40% of 40 year old white men are not perpetually choosing to be out of work, facing the full cost of that decision, to be artists, take the kids to soccer practice or even to repaint the living room walls.